✨ Value Investing Substack NEWS - TPI Is Illegal; But A Game-Changer For The EU

valueinvesting2.substack.com

✨ Value Investing Substack NEWS - TPI Is Illegal; But A Game-Changer For The EU

What's Buffett Seeing In Energy, NFLX Q2 Results, Chiplets Save Moore's Law, Myanmar Soldiers Admit Atrocities, ESG Funds Buying Big Oil, Bannon Charged with Contempt, Can China Build 7nm Without EUV?

Check out our main ASEAN value investing research blog too: Value Investing Substack!

FRONT PAGE

Highlights:

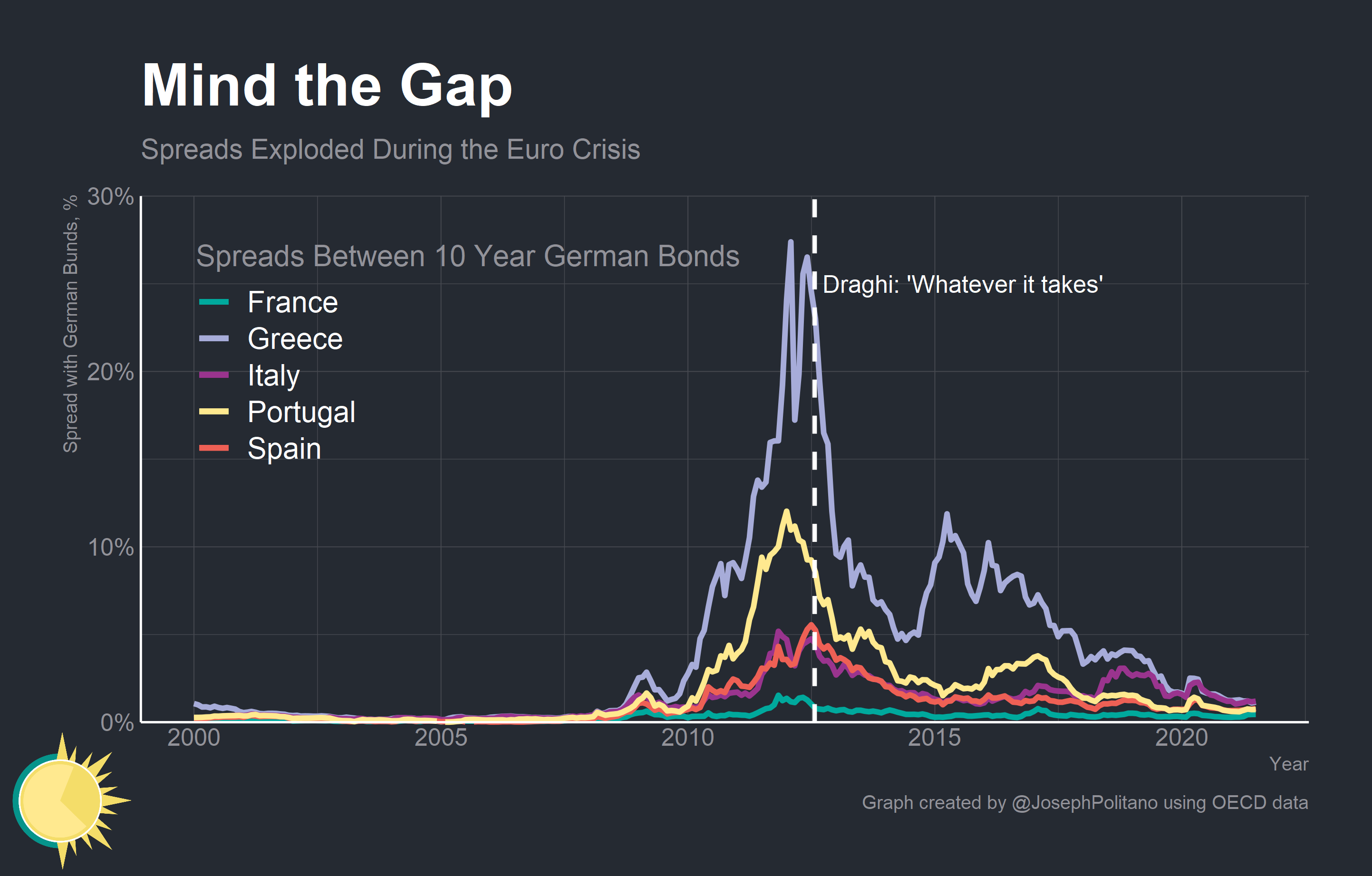

> There are two other key features of the TPI worth highlighting. First, the instrument seems to fully sidestep the capital key that the ECB’s usual bond-buying programs are supposed to abide by. The capital key basically says that the ECB should purchase bonds from all member nations in proportion to their size within the bloc’s economy—and since the TPI implicitly targets only distressed debt securities it cannot be compatible with the capital key. That’s a big deal considering how much the capital key constrained the ECB during the latter part of the 2010s and during the pandemic—the central bank had essentially purchased all available outstanding German debt and was left without enough wiggle room to support nations like Italy. If the TPI survives legal challenges, it will essentially allow the ECB to direct support on a country-by-country basis.

> The second key feature is that the bond purchases under the TPI are supposed to be neutralized on the ECB’s balance sheet. In other words, for every Euro of Italian or Greek bonds bought by the ECB under the TPI another Euro’s worth of other bonds will be sold to offset. Theoretically, this allows the ECB to transmute risky Italian debt into safe German debt by buying Italian bonds and selling German bonds. Even better, the ECB could transmute Italian debt into EU debt by selling some of the common EU debt from the Next Generation EU and SURE programs that the ECB bought during the pandemic.

> That is, however, the oversimplified and optimistic take. In practice the ECB does not need to even use the TPI—it just needs to convince markets that it is serious about closing spreads and has the firepower to back up that commitment. On that mark the ECB seems to be faltering—spreads contracted since the announcement of an anti-fragmentation tool but remain higher than at any point since the initial spike at the beginning of the pandemic. Markets seem to interpret the ECB’s goals as closer to “we will intervene in the event of an acute crisis in the sovereign bond market” than “we want to actively and preventatively close bond spreads.”

> Still, nothing is as permanent as a temporary ECB program. Monetary and fiscal policy tools in the Eurozone have a tendency to be enacted in times of crisis and generally grow into full-fledged programs through bureaucratic creep. There’s a plausible future where the TPI grows into a standing system for regulating or preventing bond spreads—and this system thereby leads to stronger, more coordinated macroeconomic policy within the Eurozone.

SUBSTACKS + LONG-READS + TWEETS

Netflix, $NFLX, co-chief executive officer has blamed the loss of 200,000 subscribers in the first quarter on inflation that’s prompted households to reduce spending.

LINKS

Stock Markets:

Chiplets helped save AMD. They might also help save Moore’s law and head off an energy crisis.

We Need to Keep Building Houses, Even if No One Wants to Buy

China's largest foundry raises alarm with production of basic 7nm SoCs

Macro

America:

In March 2021, Paul Pelosi exercised options to purchase 25,000 Microsoft shares worth more than $5 million. Less than two weeks later, the U.S. Army disclosed a $21.9 billion deal to buy augmented reality headsets from Microsoft. Shares of the company rose sharply after the deal was announced.

For his latest purchase in June, Paul Pelosi bought up to $5 million in stock options (equal to 20,000 shares) of Nvidia, a leading semiconductor company. The purchase, first reported by The Daily Caller, comes as Congress is set to vote on legislation later this month that would result in $52 billion in subsidies allocated to elevate the chip-production industry as it faces increased competition from China.

Eurozone:

Why Germany’s bond market is increasingly hard to trade | FT (2019)

ECB Hike Showcases the Death of Central Banks’ Forward Guidance

Rest of World:

MEDIA

Stock Markets & Business

Macro

Click the box above & check out our main ASEAN value investing research blog too!